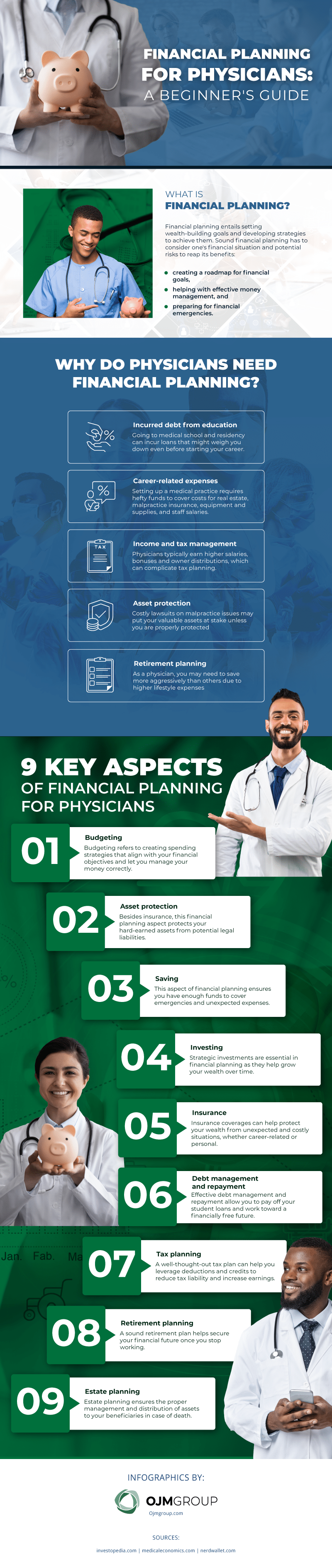

Financial Planning for Physicians

The Beginner's Guide

David B. Mandell, JD, MBA | October 24, 2024

You probably already know that physicians are among the highest-paid professionals in the US.

However, unique expenses like career-related insurance and medical school debt can put your income as a physician on the line without proper financial management.

Read below to learn more about financial planning for physicians and what you can do.

What is Financial Planning?

Financial planning is the practice of identifying your money goals and determining how to achieve them. A professional will create a sound financial plan by analyzing your:

- Income

- Expenses

- Assets

- Liabilities

- Potential risks

Financial planning lets you manage money and potential risks with your profession so you can perform your duties without worry. Some benefits of financial planning for physicians include the following:

Creates a Roadmap for Your Financial Goals

Financial planning allows you to develop concrete plans to achieve your wealth-building objectives. Whether buying equipment or saving for retirement, you can better identify priorities and set realistic goals through this process. Plus, it helps you track your progress and adjust your strategies to accommodate current circumstances.

Helps With Effective Wealth Management

Creating a budget, managing student loan debt, and identifying money-saving opportunities are all part of financial planning. They help you understand your cash flow and determine areas where you can cut expenses. In effect, you can prioritize your spending better and avoid becoming tight on cash.

Prepares You for the Unexpected

Emergencies and unexpected costs are the most significant expenses that blow through your finances. However, a financial plan can prevent this from happening.

You can set up ample emergency funds to serve as a safety net in case of equipment repairs, insurance claims, etc., that may affect your earnings.

Why Do Career Physicians Need a Comprehensive Financial Plan?

It is crucial that doctors make wise choices with their budgets for the following reasons:

Incurred Debt

Going through medical school and residency can be an exciting time for early-career physicians. However, debt and loans can also pile up here, leaving you with many expenses to settle even before starting your practice as a brand-new business owner.

Repaying these debts can be daunting, but solid financial planning for physicians can prevent them from weighing you down. You can stay on track with student loan payments until you eventually clear them, so you can move forward in your career without debt problems.

Career-Related Expenses

Besides medical student loans, many career-related expenditures add up quickly and cause cash flow problems. This is especially the case for physicians who own their own practice.

On top of that, other expenses like insurance payouts, medical equipment and supplies, and staff salaries may dwindle your finances. Financial planning for physicians becomes essential to ensure you can continue practicing and keep a smooth cash flow.

Income and Tax Management

As a physician, you have a complex tax situation since your compensation puts you within higher tax brackets. So, effectively planning for this expense is crucial to minimize your tax burden as a high earner.

A sound financial plan for physicians includes effective tax management strategies. Financial advisors can help you with:

- Maximizing tax-deferred retirement contributions

- Leveraging deductions

- Strategically monitoring income and expenses

This way, you keep more of your hard-earned income and ensure you do not overpay come tax time.

Asset Protection for Physicians

The unique professional risks you face can affect personal assets. For example, medical malpractice lawsuits can exceed typical insurance protection.

To avoid this, consider a financial plan that includes protection strategies to shield your assets from potential legal claims and other threats.

An experienced financial planner can help you assess risks and develop a comprehensive protection plan for peace of mind.

Learn More: Asset Protection for Doctors

Retirement Planning

Aside from the professional risks, you have to consider your unique retirement needs. On the one hand, you have high earning potential, but on the other, you might have significant educational debt. As a result, you may need to save more aggressively than other professionals to ensure a comfortable retirement.

With a financial plan, medical professionals like yourself can better understand:

- How much you need to save

- How to invest your savings

- When your ideal retirement age is

You can also prepare for potential healthcare costs in retirement. That said, retirement planning for physicians provides a secure and enjoyable retirement without worrying about insufficient funds to support your dream lifestyle.

Learn More: Doctor Benefits Starter Guide

9 Key Aspects of Financial Planning for Physicians

Here are the 9 most important factors when it comes to financial decisions for doctors:

1. Budgeting

Budgeting is about creating a spending and saving plan that reflects your financial objectives and priorities. You’ll need to keep track of your income and expenses, which can help you create realistic strategies to reach your money goals.

Plus, accurate budgeting allows you to adjust your financial plan as needed.

This aspect lets you stay within your means while also paying off debt, ordering medical supplies, or investing for retirement.

There are a variety of budgeting techniques you can use. One popular example is the 50/30/20 budget, which allocates 50% of your budget for needs, 30% for wants, and 20% for savings.

Another method is the zero-based budget, wherein you must justify all your expenses for a particular period starting from zero instead of referring to the previous budget. By the end of the period, your income minus your expenditures should be zero.

2. Saving

Saving strategies are essential to financial planning, especially when preparing for emergencies and unexpected events. For example, setting aside a portion of your income for future use ensures you have the money to cover the costs of further education, travel, etc.

You can also use your savings for long-term goals like future training or retirement.

When establishing a savings plan, determine how much and where to put money aside. Regularly reviewing your game plan is also crucial so you can adjust accordingly. With this aspect of financial planning for physicians, you can identify areas to:

- Cut costs

- Save more money

- Achieve your goals faster

3. Investing

While a savings account is necessary for future use and unexpected costs, inflation can decrease its value over time. As such, financial planning for physicians includes sound investment strategies to combat the effects of inflation on your money.

For instance, your financial plan may include purchasing stocks, bonds, or mutual funds to grow wealth. It may also combine these investment management techniques to diversify your portfolio and mitigate risks.

4. Insurance for Doctors

A financial plan offers adequate insurance coverage to protect your wealth against unforeseen circumstances.

Malpractice insurance, for instance, is critical for you as a physician. Lawsuits can be costly and even threaten your career, so it’s best to have this coverage to prevent significant losses.

Aside from career-related insurance, financial plans also include personal ones. For example, permanent life insurance can be a worthwhile investment to ensure physician families are cared for in the event of untimely death.

Since there are several insurance options with different premiums, working with a financial planner can help you obtain the appropriate coverage for your needs.

Related: The Beginner’s Guide to Permanent Life Insurance for Physicians

5. Debt Management and Repayment

Debt is a common issue many physicians face, especially with the cost of education and the expenses that go along with setting up a medical practice. 73% of medical school graduates have educational debt. Again, these debts can accumulate and weigh you down as you start your career.

Financial planning for physicians typically includes debt management and repayment programs to help settle these expenses effectively. With a solid plan, you can reduce financial stress and work toward a debt-free future.

6. Asset Protection

You may accumulate properties, investments, and retirement funds as your career progresses. However, these assets can be at risk if you face legal action.

As such, an ideal financial plan for physicians like yourself may consist of asset protection strategies — including limited liability companies (LLCs), trusts, and insurance policies — that shield your possessions from potential liabilities.

This way, you can focus on your medical practice with peace of mind, knowing your assets are secure and protected.

7. Tax Planning

Since higher tax brackets can eat into your hard-earned income, financial planners recommend various strategies to minimize tax liability. They may suggest you leverage deductions and credits or structure financial transactions more efficiently.

As a result, you can reduce your overall tax burden and allocate your savings toward other financial goals.

8. Retirement Planning

Retirement saving and planning for physicians often involves setting aside retirement income to support you when you’re no longer actively working.

It looks into several factors like healthcare costs, social security, inflation, and your current financial situation to help you set realistic goals for your future lifestyle.

See also: The Physician’s Guide to Life Insurance Retirement Plans

9. Estate Planning

Estate planning for physicians (managing and distributing your assets upon death) is as important as asset protection.

Estate planning helps your beneficiaries receive your retirement accounts and life insurance policies without the burden of significant estate taxes. By planning for your estate, you can make sure your wishes are carried out and your loved ones are cared for.

Recap

Your job as a physician means you face unique financial risks and expenses that can significantly reduce your hard-earned income without proper money and asset management.

In this regard, protecting your hard-earned money and other assets with a sound financial plan is in your best interest. This plan lets you focus on your work better, knowing your wealth and financial future are in order.

If you want to know how to secure your financial future and protect your assets, contact us at OJM Group. We specialize in financial advice for physicians nationwide.

Get a copy of our doctor-focused books for more personal finance tips and guides for physicians:

Disclosure:

OJM Group, LLC. (“OJM”) is an SEC registered investment adviser with its principal place of practice in the State of Ohio. SEC registration does not constitute an endorsement of OJM by the SEC nor does it indicate that OJM has attained a particular level of skill or ability. OJM and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisers by those states in which OJM maintains clients. OJM may only transact practice in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements. For information pertaining to the registration status of OJM, please contact OJM or refer to the Investment Adviser Public Disclosure web site www.adviserinfo.sec.gov.

For additional information about OJM, including fees and services, send for our disclosure brochure as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

This article contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized legal or tax advice, or as a recommendation of any particular security or strategy. There is no guarantee that the views and opinions expressed in this article will be appropriate for your particular circumstances. Tax law changes frequently, accordingly information presented herein is subject to change without notice. You should seek professional tax and legal advice before implementing any strategy discussed herein.